Posted on October 14, 2025 by MergerDomo

How to Value Your Business in India: 2025 Guide

Valuing your business is like finding the sweet spot on a tightrope, get it wrong, and the deal falls flat. In fact, studies show that overpricing is a killer: one analysis found 70–90% of M&A deals fail, often because someone bit off more than they could chew on price. Even big acquisitions can stall on valuation disagreements. For SME owners, a sloppy or overly optimistic price tag can scare off buyers or leave money on the table. In short, knowing your company’s true worth from the start is absolutely crucial. If you set a price too high, buyers won’t bite; too low, and you sell yourself short. Here are two industry-verified methods for detecting your actual business valuation. Method 1: Multiples-Based Valuation

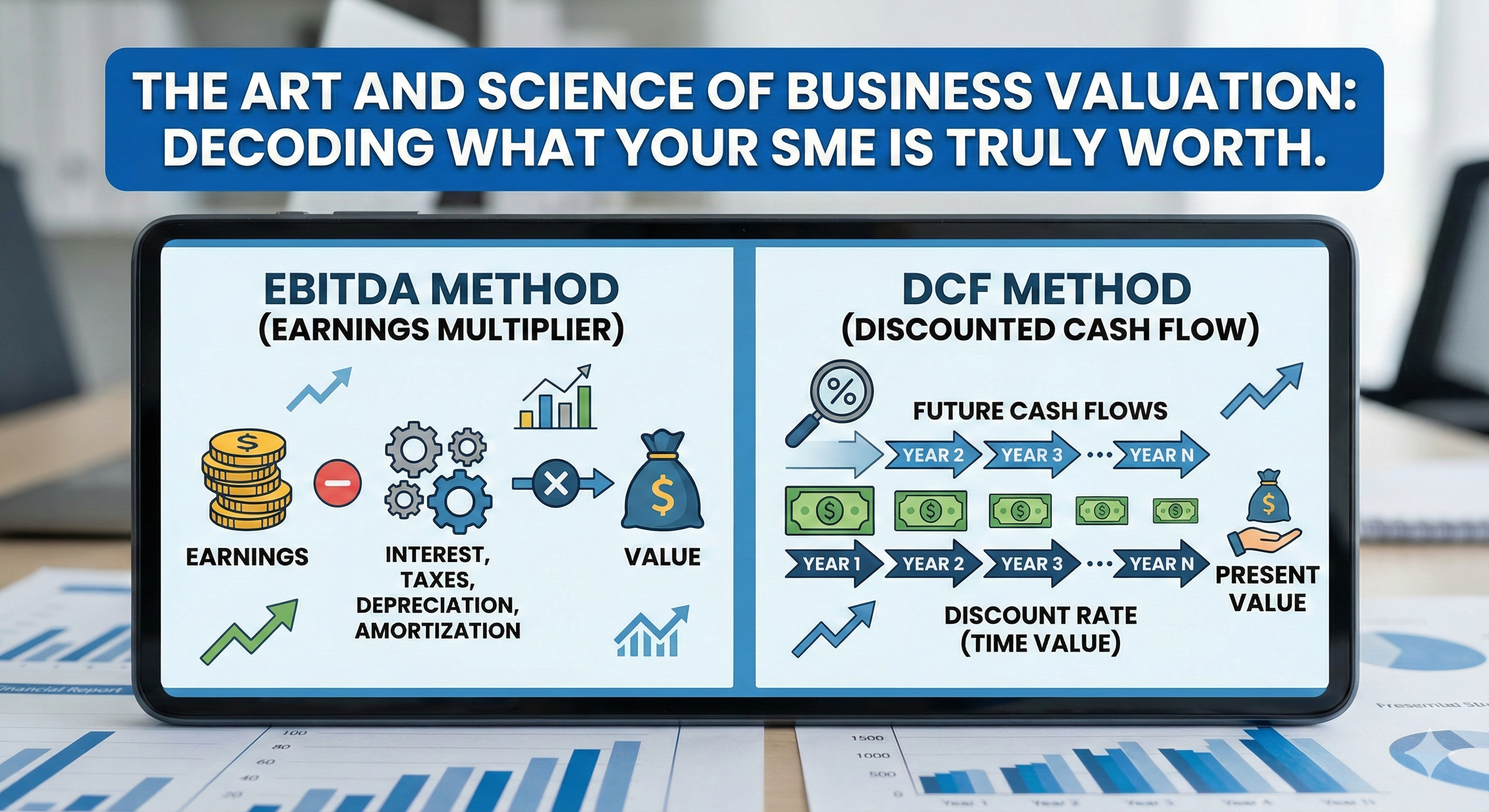

One of the simplest ways to value a business is by using EBITDA multiples. EBITDA (earnings before interest, taxes, depreciation and amortization) is a handy proxy for operating cash profit. The multiples approach works like this: find comparable companies in your industry and see what price-to-EBITDA ratio they command, then apply that “industry multiple” to your own EBITDA.

For example, manufacturing and industrial businesses often trade at roughly mid-to-high single-digit multiples. In India, auto and engineering firms typically fetch around 10–15× EBITDA. (One report cites Indian auto parts companies at ~14.5× and automobile makers at ~12.5× EV/EBITDA, while sector analysts note auto ancillary firms around 7.5–9×.) In contrast, high-growth tech or software firms may command much higher multiples (often 20× or more).

Using multiples is like using a “speedometer” for value. For instance, if your SME makes ₹1 crore EBITDA and your sector’s going multiple is 10×, your company’s enterprise value is roughly ₹10 crore.

To put it in lay terms: Profit × Market Rate = Valuation.

You might say, “Similar companies in our field sell at about 8–12× EBITDA. So at ₹50 lakhs EBITDA, that suggests a value in the ₹4–6 crore ballpark.” This method is fast and grounded in market reality, but it depends on good comparables. Always use current India-specific multiples, since local market conditions can differ.

Method 2: Discounted Cash Flow (DCF) Method

The Discounted Cash Flow (DCF) method is more like a long-range calculation. Here, you forecast your business’s future free cash flows (cash profits) year by year and then discount them back to the present value using a required rate of return (to account for risk and the time value of money). In plain English, DCF asks, “If I expect to earn X rupees each future year, how much is that worth in today’s money?”

A simple way to think of DCF: imagine your business will generate a steady ₹50 lakh profit every year for 5 years, and you use a 10% annual discount rate. You’d convert each year’s ₹50L into today’s rupees and sum them up. Five yearly ₹50L cash flows at a 10% discount rate come to about ₹1.9 crore today.

The general formula is:

DCF Value = CF₁/(1+r)¹ + CF₂/(1+r)² + ... + CFₙ/(1+r)ⁿ

where CF - cash flow for each year

and r - discount rate.

Example (for clarity):

Suppose an SME expects ₹80 lakh net cash profit next year, growing 10% yearly, for 4 years.

If you use a 12% discount rate, the DCF calculation might look like this:

Year 1 cash flow: ₹80L → Present Value approx. ₹71L

Year 2 cash flow: ₹88L → PV approx. ₹70L

Year 3 cash flow: ₹97L → PV approx. ₹69L

Year 4 cash flow: ₹107L → PV approx. ₹68L

Summing those PVs gives the estimated business value (roughly ₹2.78 crore in this example).

The disadvantage: Small businesses often have unpredictable cash flows, and estimating 5-10 years out can be tricky. But DCF forces you to spell out your assumptions, and it often catches hidden value (like long-term contracts or steady recurring revenue) that a simple multiple might miss.

Why do many SME deals get rejected? (around 60%)

Unclear or unverified financials

Investors often find that the numbers (revenues, costs, margins, cash flows) are not reliable, audited, or detailed enough.Weak promoter commitment or low credibility

Promoters (founders / owners) may have spotty track records, conflict of interest, unclear governance, or little skin in the game.Sector/market risk, limited growth or scalability

A sector might be saturated, declining, or unpredictable (regulatory risk, fast technological disruption).Valuation expectations are misaligned

Promoters may expect high valuations on optimistic growth but without backing (e.g., without customers or with high burn), which the investor cannot justify.Poor risk management, lack of differentiation

Deals may not show risk mitigation (e.g., dependency on a single customer or founder or narrow geography) or may have a lack of competitive edge.Weak business model or unit economics

If margins are thin or negative and future profitability is improbable, or if working capital issues aren’t addressed, then investors baulk.Governance, disclosure, exit concerns

How will the exit happen? Is there a path to selling or going public or being acquired? Also, is there transparency, reporting discipline, board structure, etc. All these are important factors in exit concerns.

Challenges for Indian SMEs

Valuing an SME in India has its own headwinds. Here are some common pitfalls:

Overvaluation: Many owners have a soft spot for “their baby” and set sky-high prices. This pride or optimism bias can price you out of the market. Remember, buyers will pull a dozen due-diligence rabbits out of the hat; if the base price was unrealistic, the deal often stalls.

Lack of Data: Unlike listed companies, most small businesses in India don’t have audited financials, analyst coverage, or lots of past sale data. Without clean books, you may miss hidden liabilities or mistakenly include owner perks. It’s like flying blind, one wrong input might throw off the whole valuation.

Emotional Bias: Valuation isn’t just number-crunching; it’s partly art. Yet emotions can cloud judgement. An owner might say, “I believe my brand is worth X” and ignore warning flags. In reality, buyers care about hard metrics, not heartstrings.

Even general economic conditions can skew SME valuations. For example, rising RBI interest rates raise the discount rate in DCF models, which lowers valuations. Similarly, sector trends matter: if India’s “Make in India” push is boosting electronics, then electronics SMEs might command better multiples than in downturn-hit sectors.

Here’s what investors want during an ideal SME deal 1) Verified Numbers - Investors need to reduce asymmetric information risk.Verified numbers help them model risk, estimate return, and set price/valuation.

Audited financials for the past 2-3 years; consistent accounting; clarity on revenue sources, cost structure, and margins.

Transparent cash flows and realistic projections, with scenario & sensitivity analysis.

Evidence of customer contracts, recurring revenue, pipeline, etc.

Clear working capital needs, capex, and burn rate.

Independent verification (third-party/customer references, market data) where possible.

2) Promoter Seriousness / Founder / Management Quality- Even a great idea fails if execution is weak. If promoters are casual, or lack discipline, or are unwilling to be transparent, investors see high risk. Also, promoter exit behaviour matters. (e.g., desire to exit early or via non-alignment)

Promoters with a track record, domain experience or proof of execution.

Clear commitment: equity stake, “skin in the game”, willingness to take the downside.

Good governance: clear ownership, roles, transparency; no past frauds or regulatory issues.

Strong team beyond just the founder: operational capability, management depth.

Realistic ambition and honesty in pitch: able to show both strengths and risks.

3) Sector Growth / Market Potential- Investors look for multiple-x returns, so they need potential large upside. Sectors in which growth is strong and predictable (or accelerating) are more attractive.

Growing or underpenetrated market, favorable trends (tech, regulation, customer behaviour, etc.)

Defensibility: advantages vs competitors, barriers to entry, regulatory moats or specialization.

Scalability: ability to expand geographically, into adjacent products, or via volume rather than bespoke work.

Regulatory clarity: the sector must have tolerable risk from regulation, legal constraints, and macro issues.

Demand signals: customer adoption, market size, growth projections, and evidence of traction.

Practical advice on what a “good” SME deal should do to pass the investor filter.

Financials - Clean, recent, audited, and with supporting documentation. Be ready to share customer contracts, invoices, and realistic forecast models.

Promoter resource commitment - Time, capital, past successes if any (or at least execution capability), having a good management team, structured governance, and clear alignment (equity, incentives).

Sector growth with data - Market size, growth rate, entry barriers, competitors, and regulatory risk. Show how the company can scale (e.g. geography, product line, digital channels, etc.) and how demand is trending.

Manage risk - Show what could go wrong and how you are mitigating it. E.g., dependence on one large customer, supply chain risk, regulation, technology risk, etc.

Reasonable valuation - Align valuation expectations according to current metrics. Be transparent on how much capital is needed, what the use of funds is, and what investors will get in return (exit strategy, exit time, dilution, etc.).

Try Our Free Valuation Tool

You don’t have to do all the math by hand. For an instant reality check, try MergerDomo’s free online Valuation Tool. Just enter your basic figures (annual revenue and EBITDA) and pick your industry. The tool then applies up-to-date market multiples behind the scenes, giving you an instant benchmark value.

Think of it as a virtual advisor that cuts through the grunt work. It even lets you compare using either sales or EBITDA as the base, since some sectors (like high-volume retail) may prefer revenue multiples, while others use profit multiples. The result is a ballpark valuation that you can trust or use as a reality check against your own estimates.

By using this tool, you can avoid the common trap of wildly overvaluing your company or missing factors that affect the industry. It’s a quick way to get on the same page with potential investors or buyers.

Check your valuation now. → Try our Free Valuation Tool

You can now discover deals on our website. They are verified, transparent and faster.

So you can Merge better with MergerDomo.